Iraq ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

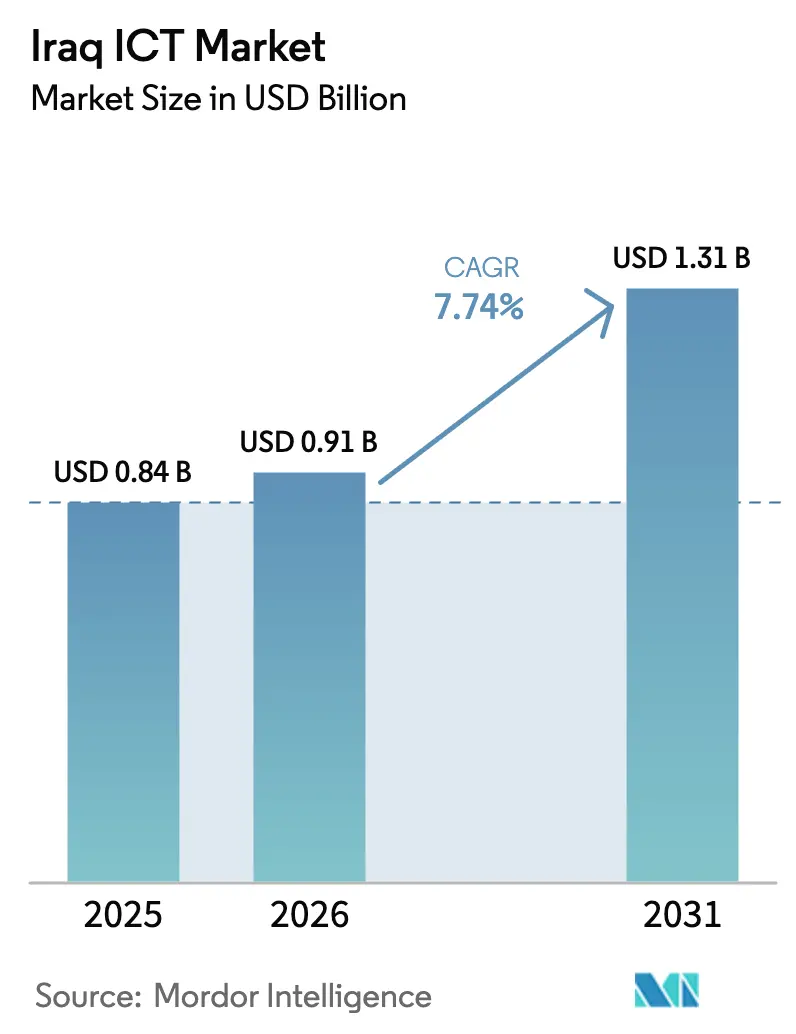

| Base Year Market Size (2025) | USD 0.84 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

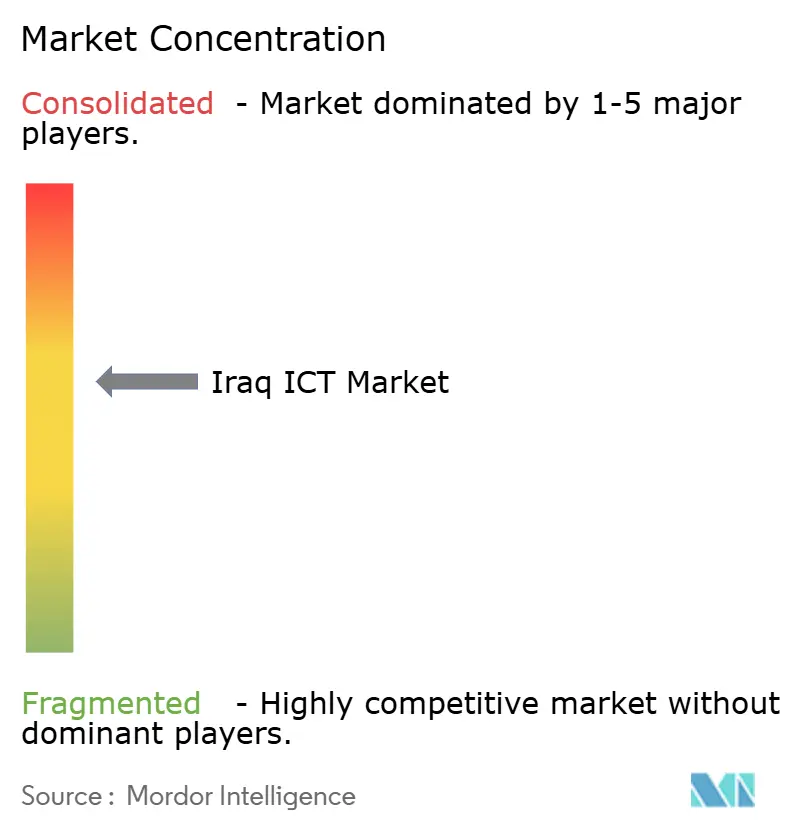

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iraq ICT Market Analysis by Mordor Intelligence

The Iraq ICT market size is expected to grow from USD 0.84 billion in 2025 to USD 0.91 billion in 2026 and is forecast to reach USD 1.31 billion by 2031 at 7.74% CAGR over 2026-2031. Growth is catalyzed by aggressive government digital programs, expanded fiber backhaul, and rising cloud uptake among oil, banking, and retail enterprise. Investments tied to the USD 17-24 billion Development Road megaproject, the newly commissioned National Data Center in Baghdad, and Iraq’s fourth submarine-cable link with Ooredoo collectively strengthen the national digital backbone. Communication Services currently anchor 37.26% of overall spending while Cloud Services record the fastest CAGR at 8.57% thanks to hybrid-cloud deployments across ministries and oil super-majors. Demand for managed security, hyperscale colocation, and IoT-enabled OT integration is rising as enterprises tackle grid instability, fiber sabotage, and cyber-espionage threats. Currency volatility and import-licensing delays for hardware persist, yet these hurdles accelerate the shift toward software-defined infrastructure and subscription-based services.

Key Report Takeaways

- By type, Communication Services led with a 36.88% share of the Iraq ICT market size in 2025.

- Cloud Services is projected to expand at an 8.12% CAGR between 2026-2031.

- By enterprise size, Large Enterprises commanded 62.15% of Iraq ICT market share in 2025, whereas SMEs show the highest projected CAGR at 8.02% through 2031.

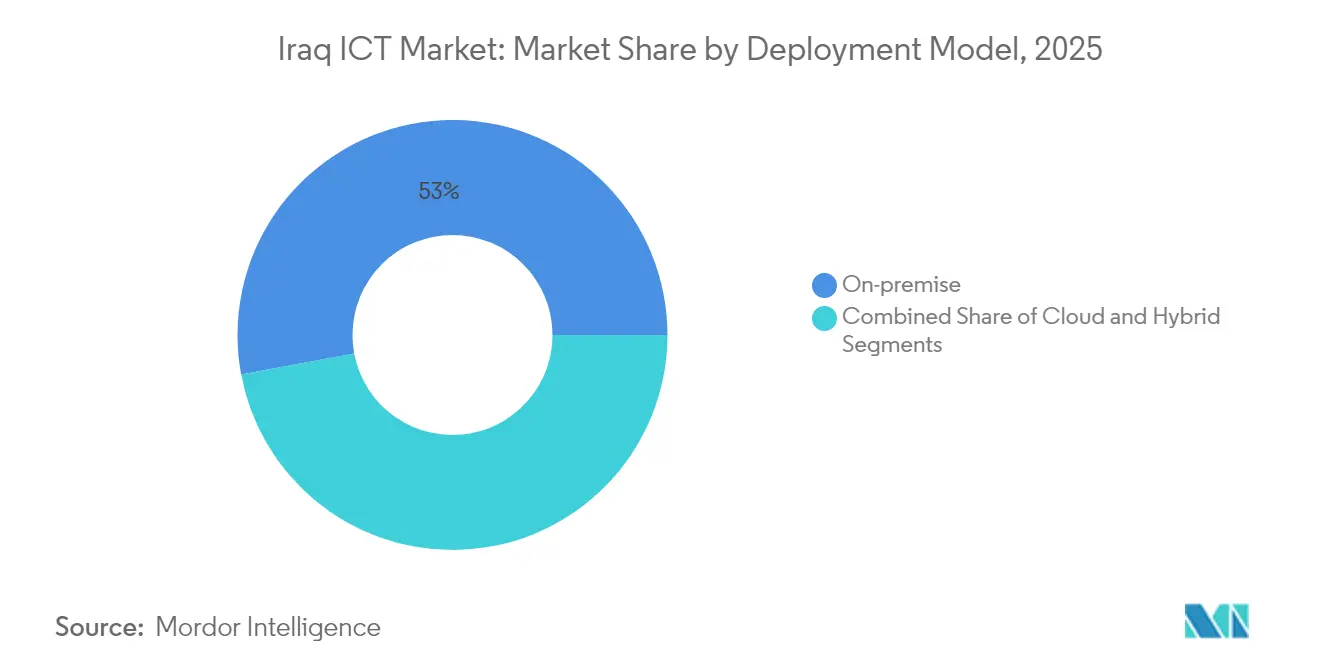

- By deployment model, On-premise solutions held a 52.95% share of the Iraq ICT market size in 2025 and Cloud deployment is advancing at a 8.62% CAGR during 2026-2031.

- By end-user vertical, Government and Public Administration captured 25.35% Iraq ICT market share in 2025, while Gaming and Esports is forecast to rise at a 8.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iraq ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digital transformation programs | +1.8% | Baghdad, Erbil, Basra | Medium term (2-4 years) |

| 5G and fiber backhaul rollout | +1.5% | Major cities nationwide | Long term (≥ 4 years) |

| Government e-services expansion | +1.2% | Federal and KRG regions | Short term (≤ 2 years) |

| Demand for managed security and SOC services | +1.0% | Oil hubs and urban centers | Medium term (2-4 years) |

| Hyperscale and colocation data-center deals | +0.9% | Baghdad, Erbil, Basra | Long term (≥ 4 years) |

| Reshoring of oil-field IT/OT spend | +0.8% | Southern oil fields, Kurdistan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital Transformation Programs

The Prime-Minister-level Business Environment Reforms Higher Committee steers coordinated e-government rollouts that include one-stop company registration, digital tax filing, and GIS-based permit systems, each triggering immediate software and integration contracts. Ministries must hook ISP DNS traffic to government infrastructure, anchoring procurement of secure DNS, API gateways, and identity-access platforms. UNICEF’s deployment of EMIS across 4,514 schools illustrates how public-sector demand scales hardware, analytics, and cloud workloads . Collectively these initiatives catalyze double-digit software and services growth within the Iraq ICT market.

5G and Fiber Backhaul Rollout

Iraq’s fourth international submarine cable and Cisco’s contract to rebuild the national backbone extend low-latency transit to Turkey and the Gulf, spurring telcos to densify metro fiber rings for 5G backhaul. The Development Road corridor will require autonomous-vehicle-ready connectivity, implying fiber trenching beyond urban zones. Private carrier FiberX is hiring FTTH engineers across Basra and Baghdad, confirming field-level acceleration. These investments make bandwidth accessible and push the Iraq ICT market toward cloud-native applications.

Demand for Managed Security and SOC Services

February 2024 sabotage of eastern Baghdad fiber cables affecting 40,000 users exposed security gaps and elevated SOC spending priorities among banks, oil firms, and ministries. Domestic players Diyar, STS, and Cyber Code scale real-time monitoring, threat intelligence, and compliance-oriented encryption, meeting governance requirements. Regional cybersecurity spending rises at 14.5% CAGR, enabling knowledge transfer partnerships that enrich local offerings.

Hyperscale and Colocation Data-Center Deals

Baghdad and Erbil attract hyperscalers seeking transit diversity and growth white space. The National Data Center already houses multiple government workloads, while private hosts negotiate power-purchase agreements and redundant grid feeds to mitigate electricity risk. New colocation capacity pulls global CDNs and financial-market platforms into Iraq, enlarging the Iraq ICT market footprint and diversifying revenue beyond connectivity resale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent grid and power-supply instability | -1.4% | Nationwide, acute in rural zones | Long term (≥ 4 years) |

| Shortage of cloud-ready Arabic-speaking talent | -0.9% | Especially Kurdistan | Medium term (2-4 years) |

| Exposure to cyber-espionage and ransomware | -0.7% | Government and oil sectors | Short term (≤ 2 years) |

| Currency and import-license volatility | -0.6% | Hardware-dependent segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Grid and Power-Supply Instability

Average Baghdad households receive fewer than 15 electricity hours daily during peak summer, forcing ISPs and data centers to run diesel gensets that raise total cost of ownership and carbon footprint. Power volatility deters hyperscalers from building Tier III facilities and obliges enterprises to locate critical workloads in hybrid arrangements. Renewable adoption through Law 53/2017 remains nascent, making energy resilience a gating factor for wider Iraq ICT market expansion.

Currency and Import-License Volatility

Central-bank foreign-currency auctions fluctuate, exposing device distributors to margin swings and delaying large-volume shipments of servers, switches, and smartphones. Import-license approvals can stretch two months and force integrators to carry buffer stock, tying up working capital. This friction channels demand toward SaaS and managed services, shifting Iraq ICT market composition away from capex-heavy hardware.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Communication Services Lead Digital Infrastructure Expansion

Communication Services accounted for 36.88% of Iraq ICT market share in 2025 on the strength of national fiber and mobile upgrades. EarthLink alone has installed 800 fiber-distribution terminals that can serve 600,000 households when fully activated. The Iraq ICT market size for Cloud Services is projected to accelerate at 8.12% CAGR as ministries and oil majors migrate ERP, HR, and analytics workloads into regional data centers. IT Services revenue grows steadily, tied to managed network and help-desk outsourcing that alleviates the local talent gap.

Currency-driven price spikes constrain IT Hardware but networking kits enjoy countercyclical demand thanks to 5G build-outs. Mandatory mobile device registration platforms and esports streaming apps spur specialized software spending. Cybersecurity suites and resilient DC infrastructure earn priority funding to counter sabotage risks, bolstering IT Security and IT Infrastructure lines within the Iraq ICT market.

By Enterprise Size: SMEs Accelerate Cloud Adoption

Large enterprises captured 62.15% Iraq ICT market share in 2025 due to multi-year government and oil contracts. However the Iraq ICT market size attributed to SMEs is expanding at an 8.02% CAGR as subscription-based ERP and SaaS pricing lowers entry barriers. Local vendor Ejaftech claims 800 clients across 1,900 projects, evidencing latent demand for Arabic-interface accounting and HR modules.

Empire World’s award-winning SAP deployment in Erbil highlights big-enterprise sophistication and showcases hybrid ERP architectures that integrate on-premise OT data with cloud analytics. SMEs gravitate toward cloud to sidestep hardware imports and to access enterprise-grade security bundles delivered via managed service providers. This behavioral shift reinforces competitive dynamics and enriches the Iraq ICT market.

By Deployment Model: Hybrid Architectures Gain Momentum

On-premise solutions retained 52.95% share in 2025 because ministries and oil operators adhere to data-sovereignty rules. Even so the cloud slice of the Iraq ICT market size will outpace at 8.62% CAGR as Oracle Cloud Infrastructure and AWS regional outposts answer compliance demands. Hybrid patterns gain traction, placing SCADA and critical data on-site while moving CX, analytics, and DR workloads into the cloud.

Areeba’s use of Oracle Cloud for payment processing illustrates compliance-ready cloud rollouts that win central-bank approval. SMEs rely almost exclusively on SaaS ERP, whereas integrated oil companies employ hybrid Hadoop clusters to crunch seismic data while adhering to national data-residency statutes. This convergence cements hybrid as the de facto architecture guiding Iraq ICT market growth.

By End-User Industry Vertical: Gaming Emerges as Growth Leader

Government and Public Administration commanded 25.35% Iraq ICT market share in 2025 on back of e-visa, land registry, and tax digitization projects. Conversely Gaming and Esports will log the fastest CAGR at 8.68% through 2031, propelled by ubiquitous 4G, anticipated 5G, and a median age under 22 years. Huawei’s 38,000-participant gaming tournament underscored monetization potential and attracted CDN and cloud-streaming investments.

In BFSI digitization of payments and neobanking apps, including fintechs featured on Forbes MENA, stimulates cybersecurity, core-banking, and AML analytics deals. Energy and Utilities modernize OT stacks around IoT, ML, and edge compute for pipeline integrity, while Retail and Logistics adopt e-commerce platforms spurred by Pure Platform’s licensing milestone. Healthcare projects funded by UNICEF roll out digital immunization records, validating telehealth and EMR demand and further diversifying the Iraq ICT market.

Geography Analysis

Baghdad anchors the Iraq ICT market with the National Data Center, telco headquarters, and the highest mobile-phone penetration at 97%. EarthLink serves 60% of national internet users from Baghdad, ensuring the city’s primacy in bandwidth and software uptak. Government SaaS procurement and SOC contracts cluster here, while multinational oil firms locate IT-OT command centers that demand redundant fiber paths and micro-segmented security.

Erbil leads the Kurdistan Regional Government zone, benefiting from earlier 4G rollout and competitive fixed-line markets via Newroz Telecom and FastLink. Separate investment codes streamline foreign ICT entry, which sustains enterprise-system deployments and data-center colocation. Summer grid deficits trigger sales of UPS, rectifiers, and power-efficient servers, shaping localized product portfolios and service-level agreements suited to KRG realities.

Basra and adjoining governorates form the southern growth axis tied to oilfield digitization and port modernization. FiberX extends FTTH and metro-ethernet links to Basra, Kut, and Karbala to meet IOC latency and uptime demands. Grand Al Faw port and the Development Road corridor will need intelligent logistics, customs clearance, and computer-vision security, injecting fresh opportunities into the Iraq ICT market while addressing regional disparities where Wasit clocks only 72% mobile-phone usage.

Competitive Landscape

State ownership of the fiber backbone through the Iraqi Telecommunications and Post Company shapes a moderately concentrated structure with regulatory gatekeeping. EarthLink’s 60% internet-user share and the triopoly of Zain, Asiacell, and Korek controlling 90% of mobile towers exemplify oligopolistic traits in connectivity segments.[1]Freedom House, “Iraq,” FREEDOMHOUSE.ORG However software, cloud, and cybersecurity remain fragmented, allowing domestic integrators E2NEXT and Diyar to win public-sector contracts and oilfield IT-OT tenders.[2]E2NEXT, “Main,” E2NEXT.COM

Strategic moves center on infrastructure alliances and portfolio diversification. Cisco’s optical-backbone rebuild, Ooredoo’s submarine-cable venture, and Oracle’s cloud region all depend on joint ventures that satisfy local ownership and data-residency norms. Telcos diversify into edtech as Zain-backed conglomerates acquire platforms such as Eduba, signaling value-chain expansion beyond pure connectivity.[3]Wamda, “Eduba acquisition,” WAMDA.COM

Emerging challengers exploit niche growth. Gaming-infrastructure providers partner with Huawei cloud, fintech developers tap API banking mandates, and Arabic-language ERP startups onboard SME clients unattainable by global suites. Heightened demand for sovereign SOC services and energy-sector OT security opens lanes for specialized Iraqi firms, ensuring the Iraq ICT market remains contested despite backbone centralization.

Iraq ICT Industry Leaders

IBM Corporation

Microsoft Corporation

Telefonaktiebolaget LM Ericsson

Oracle Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Iraq and Ooredoo finalized a fourth submarine-cable deal to bolster international transit capacity

- February 2025: ICTSI’s Basra Gateway added a 125-ton mobile harbor crane, underscoring port digital-logistics upgrades

- January 2025: FiberX began large-scale hiring for FTTH expansion in central and southern governorates

- December 2024: E2NEXT crossed 300 public- and private-sector IT projects, reflecting integrator growth

Iraq ICT Market Report Scope

ICT encompasses a spectrum of technological tools that facilitate the transmission and processing of information. The term itself is an amalgamation of information, communication, and technology. The study tracks key market parameters, underlying growth influencers, and major vendors operating in the market, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from various ICT types that are used in various industry verticals across Iraq.

The Iraqi ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of enterprises (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

What is the projected value of the Iraq ICT market by 2031?

The market is expected to reach USD 1.31 billion by 2031, expanding at an 7.74% CAGR.

Which segment is growing fastest in Iraqi ICT spending?

Cloud Services leads with an 8.12% CAGR as enterprises and ministries adopt hybrid architectures.

How big is the SME opportunity in Iraqi ICT?

SMEs’ share is rising at an 8.02% CAGR, underpinned by cloud-based ERP and SaaS uptake.

Why is Gaming and Esports a priority vertical?

A youthful demographic, 4G coverage, and high engagement 38,000 tournament participants drive a 8.68% CAGR.

What limits large-scale data-center investments in Iraq?

Chronic grid instability raises power costs and reliability concerns, deterring hyperscale builds.

How are currency swings reshaping ICT procurement?

Hardware imports face price volatility and licensing delays, prompting a shift toward SaaS and managed services.

Page last updated on: